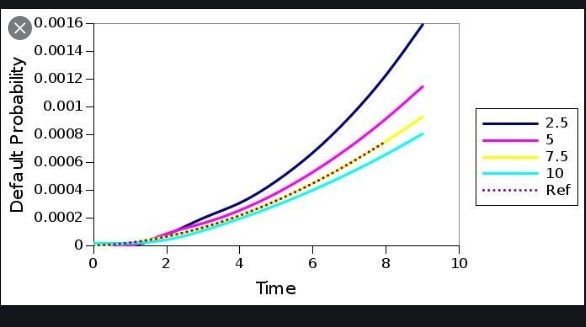

Default probability is the probability of the debtor not being able to make repayments. In the market context, it is the probability that the asset yields no returns to its holder over its lifetime with the asset price sliding to zero. Investors use this to expect loss from an investment.

It is used in a variety of credit analyses. Therefore, It is also closely linked to the expected loss which is defined as the product of the PD, the loss gave default (LGD), and the exposure at default (EAD).

Probability of default – Wikipedia

https://en.wikipedia.org › wiki › Probability_of_default

Probability of default (PD) is a financial term describing the likelihood of a default over a particular time horizon. It provides an estimate of the likelihood …

Probability of Default – Overview, Formula, Market vs. Individual

https://corporatefinanceinstitute.com › Resources

Probability of Default (PD) is the probability of a borrower defaulting on loan repayments and is used to calculate the expected loss from an investment.

Probability of default and loss have given default analysis – Abrigo

https://www.abrigo.com › blog › probability-of-default…

Probability of Default/Loss Given Default analysis is a method used by generally larger institutions to calculate expected loss.

The Probability Approach to Default Probabilities – Nicholas M …

https://kiefer.economics.cornell.edu › Probability…

by NM Kiefer · 2006 · Cited by 23 — the default probability for a risk bucket on the basis of historical information and … For very large samples all estimators work better, as.

Probability by Using the Merton Model for Structural Credit Risk

https://www.mathworks.com › help › default-probability…

The Merton model is structural because it gives a relationship between the default risk and the capital structure of the firm.

How Default Probability Works

Firstly, This is the risk that the borrower will not be able to repay its debt in full or on time. Here, the risk of default is by analyzing the obligator’s capacity. To repay the debt in terms of the agreement. The default probability is linked with financial features. Like inadequate cash flow to service debt, declining revenues or operating margins, high leverage, declining or marginal liquidity. As well as the inability to successfully implement a business plan. Added to all these factors. The willingness to repay must also be seen.

Also, It’s to verify if the default event will take place. It applies to a horizon, typically one year. Credit scores like FICO for consumers or bond ratings from S&P, Fitch, or Moody’s fir corporations, typically mean a certain probability of default.

Lastly, For group obligators who share similar credit risk features like RMBS or pool of loans, a default probability may be derived for a group of assets which is representative of the typical (average) obligor of the group. In comparison, a Default probability for a bond or loan is determined for a single entity.

High-Yield vs Low-Yield Debt

Companies that are cash-flush with low default will be able to issue debt at lower interest rates. Investors who are trading these bonds on the open market will price them at a premium as compared to riskier debt. It simply implies that safer bonds will have a lower yield.

lastly, Where a company’s financial health takes a turn for the worse over time, investors in the bond market will adjust to the risk and trade the bonds at lower prices and give higher yields. High-yield bonds are known to have a high default and thus pay a high yield or interest rate. At the other end are state bonds like U.S. Treasury bills, which usually pay the lowest yields and have the lowest risk of default; the state can always print more money to have the debt paid.

Social Media: Facebook, Twitter, Wikipedia, LinkedIn, Pinterest