What is a Credit Score?

A credit score is a scoring system that lenders use in order to decide whether or not to extend credit to you. Your credit score can also be used to help decide the terms that you are offered or the rate you have to pay for them.

Your credit score contains information about you and your credit experiences, like your bill-paying history, the number, and the type of accounts you have. Whether you pay your bills by the due date, collection actions, outstanding debt, as well as the age of your accounts, is collected from your credit report. With the aid of a statistical program, creditors compare this information to the loan repayment history of consumers with similar profiles.

A credit scoring system awards points for each factor which helps in predicting who is most likely to repay a debt. A total number of points of a credit score helps predict how creditworthy you are: how likely it is that you will repay a loan and make the payments when they are due.

Some insurance companies on the other hand, also use credit report information, along with other factors, in helping to predict your likelihood of filing an insurance claim as well as the amount of the claim. They can consider this information when deciding whether to grant you insurance and the amount of the premium they charge. The credit scores insurance companies use sometimes are known as “insurance scores” or “credit-based insurance scores”.

How Is Your Credit Score Determined? – Experian

https://www.experian.com › blogs › ask-experian › ho…

Credit scores are determined by different categories, with payment history as the most important. Learn more about the factors that affect

What Affects Your Credit Scores? – Experian

https://www.experian.com › ask-experian › score-basics

From payment history to credit utilization, learn which factors affect your credit and how service accounts can now positively impact your credit score

How to Improve Your Credit Score Fast – Experian

https://www.experian.com › blogs › improving-credit

It’s possible to improve your credit scores by following a few simple steps, including: opening accounts that report to the credit bureaus, maintaining low …

How To Improve Your Credit Score | Bankrate

https://www.bankrate.com › Authors › Michelle Black

Here’s a breakdown of how credit scores work along with some tips you can use to try to boost these important numbers.

Who Determines Your Credit Score?

The two primary scoring models are FICO and VantageScore. FICO was created in 1989 by Fair, Isaac, and Company.

VantageScore was created in 2006 as a joint effort by the three major credit bureaus and was created to be a more consumer-friendly model of credit scoring.

FICO

FICO makes use of predictive analytics to take consumer information and analyze it. The company uses the following five factors for its credit scoring model:

- Payment history

- Total debt

- Credit history

- Types of credit

- Credit inquiries.

From these factors, FICO gives each individual a credit score. To generate a FICO score, you must have a certain amount of available credit.

On the whole, FICO is considered a credible source of consumer information. This is because FICO scores tend to be a reliable way of determining if someone will be able to repay a loan on time.

VantageScore

VantageScore was developed as a joint venture by Experian, Equifax, and TransUnion. It calculates consumer credit scores just like FICO but in a slightly different way.

Unlike FICO, VantageScore uses six different categories in its credit scoring model, they are:

- Payment history

- Credit utilization

- Total balance

- Depth of credit

- Recent credit

- Available credit.

How to Improve Your Credit Score

Check Your Credit Score

By checking your credit score, you will actually know where you stand credit-wise. You can do this by getting copies of your full credit reports from all three bureaus which are Experian, Equifax, and TransUnion. You can get your reports for free once a year at www.annualcreditreport.com or by calling other websites who offer free credit score check, even though the Federal Trade Commission (FTC) actually warns against these offers which are deceptive.

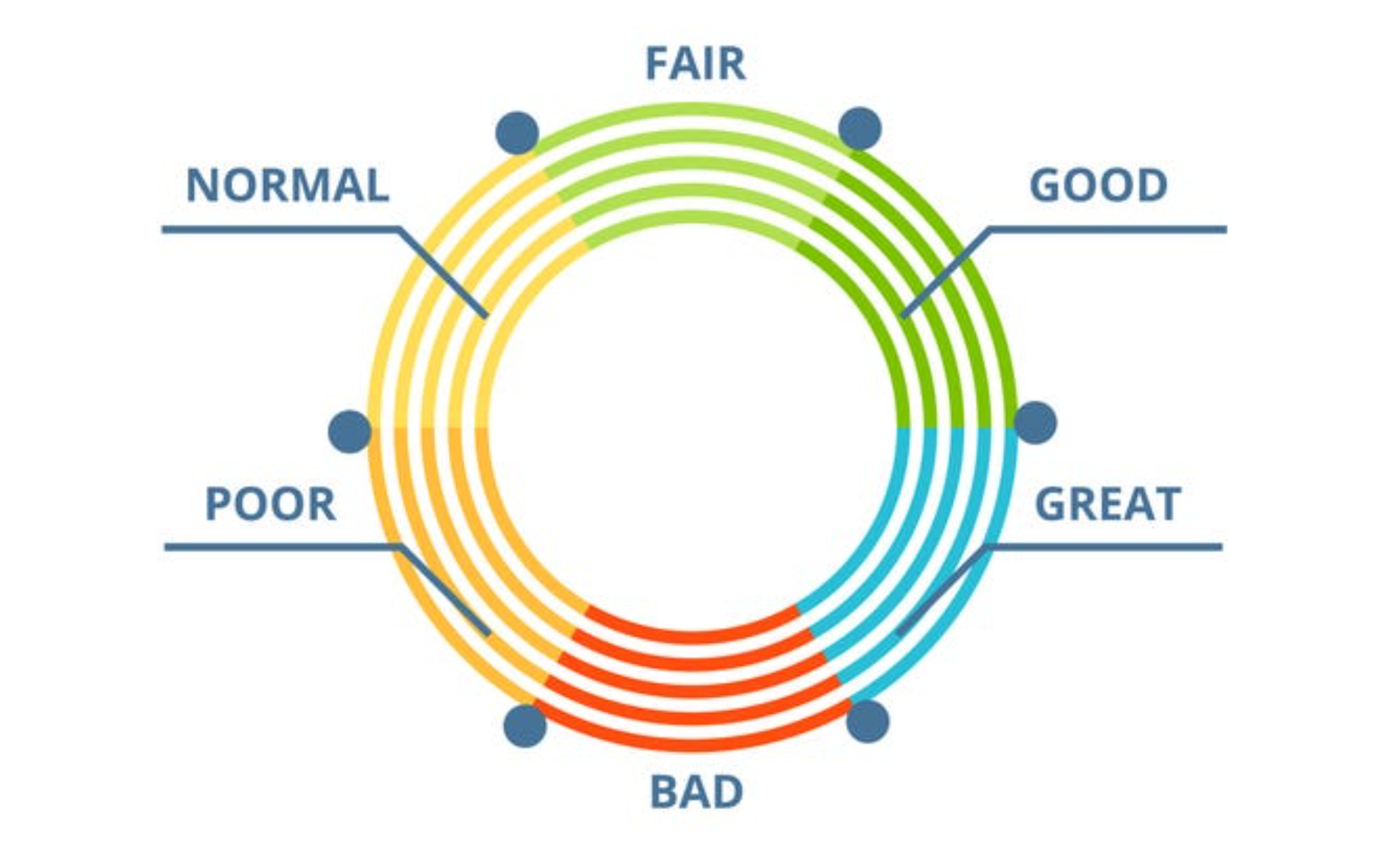

The credit score ranges from 300 – 850. A good score is between 700 – 740, depending on the scoring model in use. If you fall into this category, you are qualified for the best credit cards and the lowest mortgage rates.

Despite Errors If You Find Any

If you find incorrect information on your credit report, you have to dispute it to avoid it affecting your score. Even though errors are not common they sometimes happen.

To clean up incorrect information from your file do this:

Once you have a copy of your full credit report handy, check your identity information (social security number, the spelling of your name and address) as well as your credit history.

Review the list of credit cards, outstanding debts, and other major purchases. If you spot any mistakes or questionable items, make a copy of the report and highlight the error.

Gather any information you have to back you up like bank account statements, and make copies of them, then write a letter to the specific credit reporting agency where the incorrect information came from.

Don’t Spend More Than You Earn

You must ensure that you don’t spend more than you earn. To do this, you can create a budget for yourself and work with it.

Make On-Time Bill Payments

Pay your bills on time if you want to fix bad credit. If you are behind any bill, try to pay it as soon as you can. Making on-time payments are the single most important factor in your credit score. Thus your credit won’t improve until you consistently pay your bills on time.

Pay Down Credit Card Balances

Where you have any outstanding balances, you have to draft out a budget on how you can pay down these debts. You can do this bit by bit every month until you are done paying.

Make sure you know your credit limit and ensure that you stay well under the maximum when charging items. Try to pay down debts instead of canceling them. The total amount of available credit affects your score even when you owe nothing.

Don’t Apply for New Credit

Try as much as you can to avoid opening a new credit card. Each time you apply for credit, it gets listed on your credit report as a “hard inquiry” and having too many within two years puts your credit score in jeopardy.

Social Media: Facebook, Twitter, Wikipedia, LinkedIn, Pinterest